Today I’m sharing with you a graph that I show during “The Graduate Student and Postdoc’s Guide to Personal Finance.” It’s always shocking to the audience. It motivates some people to save during grad school and some people think it’s unreasonable; I’ll break all of that down here.

The point of this graph is to illustrate the power of compound interest, which roughly translates to investment returns. (More on that ‘roughly’ later!) I used Illuminations to create the graph.

Here’s the toy example:

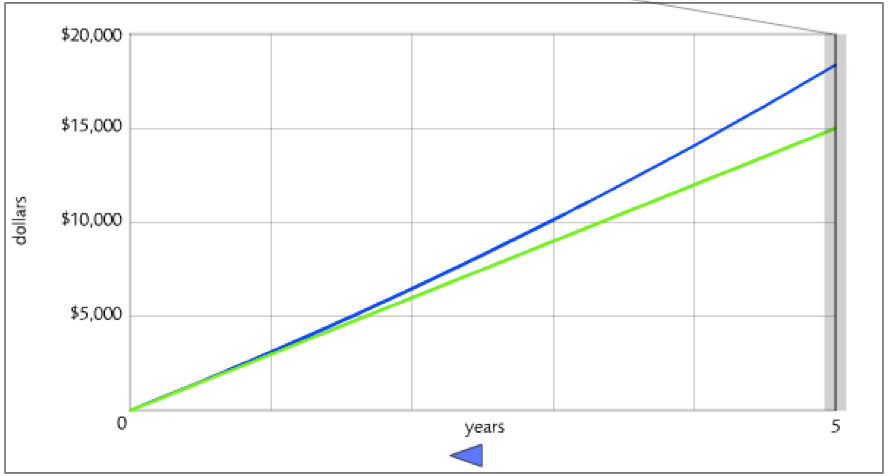

Alana receives a $30,000 per year stipend and she saves 10% of it consistently into an IRA that is invested for her retirement (i.e., rather aggressively). So she is saving $250/month every month throughout her five years in graduate school. Her investments generate an average annual rate of return of 8%.

Over those five years, Alana puts in $15,000 and her ending balance is $18,369.21. So that’s cool and all – an extra $3k.

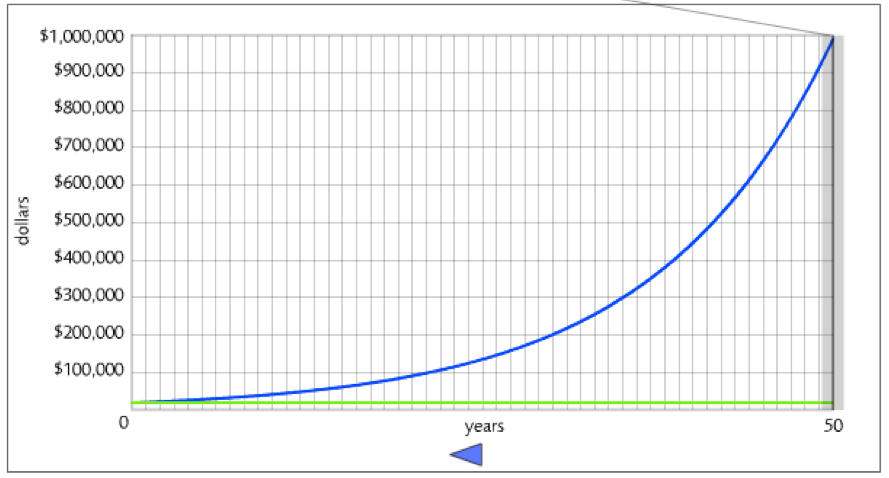

But then, she keeps the money invested for the same average rate of return for the next fifty years. So if she graduates when she’s 30, she checks her balance again at age 80. Remember, she’s not making additional contributions to this money at all – it’s just what she saved during grad school.

Alana’s investment balance has grown to a breath-taking $989,688.35! Her diligence to save during grad school translates to an extra $1M in retirement!!

I really want you to let that exercise sink in. That is the power of compound interest. Even a modest amount of money, given enough time and a high enough rate of return, can turn into an enormous amount of money! That is why any small amount of money that you can invest during grad school will have a huge impact on your long-term financial wellbeing.

I hope you had a “wow” moment there and are motivated to start investing or increase your investing (or pay off debt). I’m going to break down the exercise now to address the common questions and objections that I hear.

Free 10,000-Word Email Course on Investing for Early-Career PhDs

Subscribe to our mailing list to receive the 6-day email course designed for graduate students, postdocs, and PhDs in their first Real Jobs.

1) It’s unreasonable for a grad student to save $250/month.

Whether or not saving $250/month is possible or reasonable is highly individual and depends both on the grad student’s income (usually a stipend rate set by the university/department) and personal living expenses. $250 is absolutely possible for many grad students (by the end of our PhDs – after lots of optimization – my husband and I were saving about $800/month together), and it’s not for others. Sometimes stipends are just too low, the local cost of living is just too high, or you have a challenging situation like paying off a lot of debt or supporting family members.

I do think 10% or $250/month are good benchmarks for grad students who have the ability to save. If they’re not saving that much yet, this illustration should encourage them to find a way to save more. If they’re already at that level, they can feel good about their efforts and maybe push for more as well.

The point of the exercise is not to say you have to save $250/month or it’s all useless. It’s to illustrate that saving early – whether it’s $250/month or $25/month, whether it’s every month or in one lump sum – has an incredible impact on your wealth over the long term. So any amount you can invest during grad school is wonderful. At just $25/month, that ending balance is nearly $100,000 – an amazing amount of money as well!

2) A guaranteed 8% rate of return isn’t available.

The objection to the 8% average rate of return figure is two-fold: 1) Why 8%? 2) You can’t get a high fixed rate of return in today’s market.

The reason investment returns are illustrated using compound interest is to make the math easier and keep the point clear. If you looked at models that include how the stock market really behaves, they get complicated and difficult to parse. You don’t end up with a nice single value but rather a distribution of possible results. There is a chance (minuscule over long periods of time, but non-zero) that you could lose all your money. There is an equally small chance that you end up a billionaire. And everything in between. But somewhere in the big fat middle of that distribution is the answer that a clean compound interest calculation gets you to.

The point of the exercise is not to predict exactly how much money you’re going to end up with in retirement down to the cent. It’s to show you the scale of change that’s possible over a long period of time with a reasonably high rate of return and motivate you to harness the power of compound interest.

If you look at enough of these types of compound interest examples, you’ll see a few different interest rates chosen. When we’re talking about stock investments, 8% is on the modest side. The long-term average return for the total stock market is often pegged at 10%, so that’s a popular figure. Dave Ramsey likes to use 12%. I chose 8% because it’s reflective of a largely-but-not-completely stock investment portfolio, which is appropriate for aggressive long-term investing (not speculating). It’s also pretty unlikely that you would have a single expected average rate of return over 50 years, as the standard advice is to move toward more conservative investments as retirement draws nearer, but the illustration ignores that detail as well. If the stock market future more or less resembles its past, 8% is a very achievable long-term average rate.

To really blow your mind, the same example above with a 12% rate of return gives an ending balance of $7,192,995.42. So this rate of return choice really matters to the illustration, and even the breath-taking ending balance I got to is a conservative example of the power of compound interest.

3) I don’t want to wait 50 years to retire.

I actually have never heard this objection from an audience member, but it’s one I have in my own mind. When I break the news that we’re looking at a 50-year compounding period, I say “So if you get out of grad school when you’re 30, you’re now 80. But don’t worry because by then 80 will be the new 50.” There’s some truth to that; people are living longer, and Ray Kurzweil thinks that by 2029 it may be possible to live forever.

There’s no special reason to use 50 years in this example, except that it’s a round number that when added to a grad student’s age puts them past the current retirement age but probably still kicking. The point is that the more years you give compound interest to work, the more impressive the outcome. It really does matter whether you start saving during grad school or after! If you’re shooting for a specific number that represents financial independence, starting earlier gets you there earlier.

Free Email Course: Investing for Early-Career PhDs

Sign up for the mailing list to receive the free 10,000-word email course designed for graduate students, postdocs, and PhDs in their first Real Jobs.

4) You’re not accounting for inflation.

Good catch! $1M in today’s money is very different from $1M in 2067 money. It won’t seem nearly so impressive at that point. But that should not stop you from saving. If anything, the existence of long-term inflation (in the US, a bit higher than 3% annually on average) argues for more saving and more aggressive investing. You are losing purchasing power if you keep it in cash and barely maintaining it using bonds.

5) Can’t I achieve the same result by maxing out my 401(k) in my first year with a real job?

I fielded this question only once, and it was during my very first seminar ever. And it’s a great one. My argument is that you come out of grad school with $18k in savings and continue to invest that for 50 years. Currently, the maximum someone under the age of 50 can contribute to a 401(k) is $18,000 per year. The point is correct: If you just max out your 401(k) in your first year with a real job and keep it invested for 50 years, you get the same outcome as you would by saving that $250/month all through grad school. The compound interest math is identical.

But guess what’s even better? Saving $250/month during grad school and maxing out your 401(k) in your first year with a real job – and every year after. And who is more likely to max out their 401(k) (no mean feat!): someone who has never saved a dime or someone who is already in the habit of saving, even in a challenging time of life like grad school?

Becoming a mega-saver with your first real job is a great step. But it doesn’t erase the opportunity you have to start investing during grad school. You can have your $1M in retirement from that first year’s 401(k) and your $1M from grad school.

Free 10,000-Word Email Course on Investing for Early-Career PhDs

Subscribe to our mailing list to receive the 6-day email course designed for graduate students, postdocs, and PhDs in their first Real Jobs.

[…] Whether You Save During Graduate School Can Have a $1,000,000 Effect on Your Retirement […]